A 21st Century Model for Financing Homeownership

Shared equity investments like Homium are a way for institutional investors to partner side-by-side with working families and local governments to bolster homeownership and middle-class wealth creation, while reducing housing inequity and displacement.

Single family homeownership is the foundation of middle-class financial security and a primary feature of the American Dream. Enabling first-time homebuyers through guaranteed mortgages and rewarding them with interest deductions has been a goal of American economic policy since FDR’s New Deal. Access to homeownership and equitable home financing have served as the ladder to the middle-class for generations of Americans. By contrast, those who were denied equal access to that ladder by discriminatory policies and lending practices still struggle to catch up. Homeownership and the policies which enable it shapes our neighborhoods, our cities, and our markets. The middle class that formed around homeownership still stands as the accessible and replicable economic success story that motivates millions to save their wages with the hope that someday, they too might buy a home of their own.

The way that single family homes are financed is changing. After the collapse of the US housing market in 2008 and the global financial crisis that followed, state governments and federal agencies overhauled the rules that govern home financing, to reign in the abuses that led to systemic risk and widespread foreclosures. These changes have largely purged the market of exotic debt products which tipped off the toxic asset bust. Predatory lending is less prevalent now than before the crisis, interest rates remain near historic lows, and new financial and real estate technology is making it easier than ever for credit-worthy borrowers to find simple-to-understand home financing.

Despite these improvements, homeownership among young adults fell from 45.0% to 37.0% from 1990 to 2015, slightly rising to 41.6% in 2021. But this recent increase masks a deeper issue: more young adults now live with parents or others, delaying independent household formation. The share living with parents rose from 12.5% to 20.2%, and with others from 10.7% to 18.3%. Many more young adults with good incomes miss out on building wealth in a home of their own, but also delay the formation of families and mutual savings that will be counted on down the line and are the true basis for financial and social security.

Younger Americans are not the only potential homebuyers missing out. Buyers enjoy low interest rates and near full employment but a housing market that is nonetheless unaffordable to many, if not most, wage earners. Even those with savings, steady income, and good credit are facing housing markets with increasingly steep barriers to entry and the frustration of losing a bid to an all-cash offer from another well-heeled buyer looking to turn a single-family house into a rental income property.

One difference from previous eras is that today’s homeowners must contend with increasing competition from private equity and institutional investors for limited housing stock in desirable neighborhoods. As of early summer 2023, these investors represented about 26% of all single-family home purchases in the U.S., a slight decrease from earlier in the year but still significantly higher than pre-pandemic levels. The trend has shifted towards smaller investors, with those owning three to nine properties comprising 47% of investor purchases by June 2023, the highest proportion since 2011.

Who can blame them? Home values in the United States have recovered from the crash to reach those highs in just ten years, even with sluggish global growth. Years of quantitative easing, combined with housing supply constraints and generational differences in wealth, income and consumer habits have created a ripe environment for the commercialization of housing. This is especially true in California, where nearly a quarter of single-family homes and condos are bought in all-cash transactions, a leading sign that a medium or large scale investor has made the purchase. Even as interest rates have climbed, the consolidation of commercial real estate has not shown its equal in residential markets, suggesting there are secular forces keeping the cost of housing high.

The Home Affordability Crisis

According to Redfin, it is 50% less expensive to rent a starter home in Los Angeles than it is to purchase one and pay the associated monthly mortgage payment. This is in a city and county where nearly half of residents pay 35% of their income toward housing or are simply moving elsewhere, and more than 75,000 are homeless, in no small part due to pressures from all-time high and rapidly growing rents.

Large cities are not the only place in California where housing is hard to come by. According to the California Association of Realtors, the minimum income required to purchase a single-family home in the state has more than tripled since its low in 2012, from $56,320 to $208,000 in Q2 2023. The Inland Empire, previously more affordable, now requires a minimum income of $142,800, compared to $326,000 in the greater San Francisco Bay Area. However, incomes in rural areas remain lower and grow slower than those in urban centers. The median Inland Empire worker, earning just over $41,000, still falls short of the median income in the US as a whole.

Homeownership rates fell in the US by 5.6% from 2004–2016, and though they have ticked up in recent years, they remain below rates from 30 years ago for everyone except for households over 65 years old. Average families in California simply cannot afford to become homeowners at the scale that policymakers and society at-large seem to expect, given that homeowners are given special benefits and tax protections to encourage their flourishing. Homeowners have closer bonds with their neighborhoods and local institutions, such as schools, churches, businesses, and municipal governments. Stable housing and financial uplift leads to improved outcomes for everyone. Homeowners take greater pride in the place where they live and contribute more of their own social and financial capital in developing their property and relationships with neighbors. Those relationships become strong and resilient communities. Homeownership is not an ideal that we can afford to let further out of reach.

Home Lending Today

Following the 2008 crisis, Fannie Mae and Freddie Mac were taken into conservatorship by the US Treasury, where they remain today. The reform of mortgage lending regulations after the crisis dramatically limited the kind of risky mortgage products that were prevalent from 2001–2007, such as negative amortization loans, or loans to borrowers with little or no ability to repay them. Compared to that era, the lending market has stabilized as housing prices recovered and boomed again, and borrowers with good credit and high income have little trouble finding credit albeit at higher interest rates than in previous years.

But the industry and homeownership as an institution today benefits a shrinking part of the population. Families who purchased homes long before the crisis have enjoyed rising equity and low interest rates for refinance. Those who bought in the run-up have recovered the losses they weathered through the down years. But borrowing against your home, even in times of plenty, means a higher mortgage payment every month, when for even credit-worthy borrowers, inflation-adjusted wages in the US have only increased by 9.7% since 1979. Major expenses, such as childcare and education, healthcare, and ever-present student loans crowd out the income available to pay for additional housing costs, leaving homeowners unable to access their equity.

Some lenders will be tempted to resort to predatory debt products that hide their costs through negative amortization or surprise balloon payments, the kind of built-in risk that led to so many foreclosures when home values fell and unemployment spiked. Regulators will do their best to prevent the kind of systemic risk that could cause those conditions again, creating a tension between homeowner liquidity and responsible underwriting standards. Additional leverage and payment obligations put a strain on borrower credit ratings, negatively affecting the value of mortgages on the secondary market and the government sponsored entities which back those mortgages.

These conditions could also give rise to restrictive equity line products such as reverse mortgages or purchase option contracts which purport to come with no monthly payments, but reserve an outsized share of the value of a borrower’s home—sometimes with an obligation to sell or refinance to pay off the debt at an inconvenient time, or immediately following the death of a loved one. Without a way to tap their home equity that does not increase their monthly debt burden, many homeowners will forfeit all their future appreciation for short term liquidity by simply selling their home, often to an investor who will turn it into a rental property.

Absent some solution or a sudden spike in wage growth (a change made unlikely by globalization and automation), this imbalance between the affordability of homes and the availability of rising income to pay debt service on mortgages will continue to erode the possibility of homeownership, particularly for younger working people. That goal — a home with four walls your family can call their own — will be a pipe dream for all but the most fortunate Americans. Those who cannot enter the homeownership stream will more and more rent their homes from increasingly consolidated institutional ownership conglomerates, remote investor groups who will decide how and when capital is deployed, to which neighborhoods, based on calculations made far from where their consequences are felt.

Economists and policymakers know that the answer isn’t to resist some perceived intrusion of capital into these housing markets. Quite the contrary, most policymakers and foundations know that investor capital can transform neighborhoods and local business districts for the better without displacing the people who live in them. The key is to improve the financial circumstances of those same people by increasing access to high paying jobs, low-cost credit, and quality education and public services. Investors are hungry for exposure to home values in neighborhoods with growing, thriving populations, but the mechanisms necessary to connect capital to these opportunities do not exist until we invent them.

A New Home Finance Stack

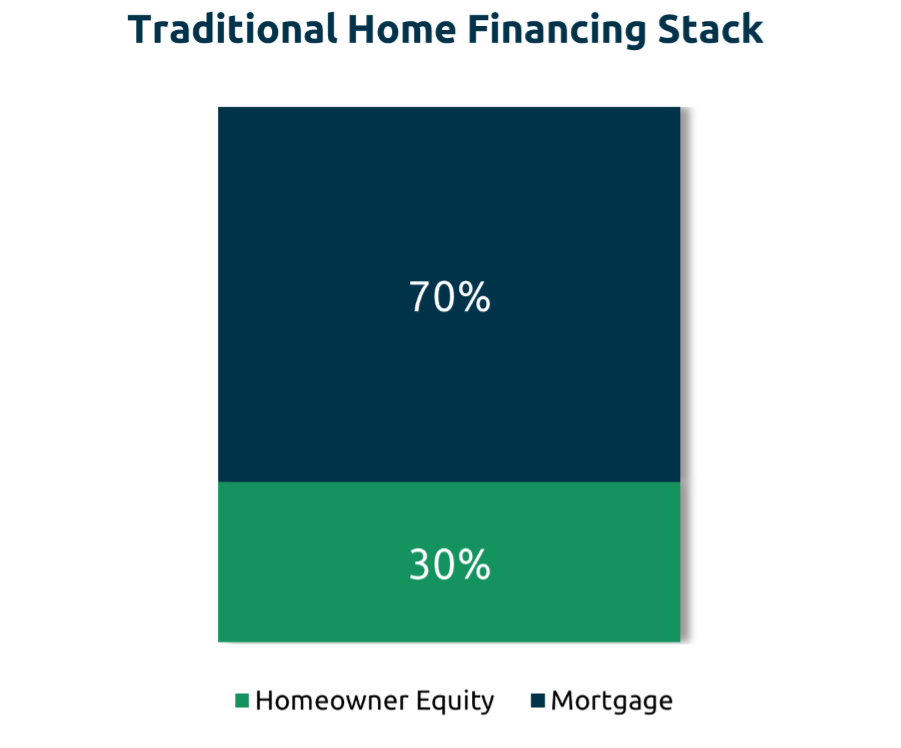

Part of what makes homeownership and home lending less flexible than commercial real estate finance is that only one type of equity comprises the finance stack of an owner-occupied home: the homeowner’s. Any outside participation in the financing of a home takes the form of debt, usually with a fixed rate mortgage, and sometimes a second mortgage with a slightly higher rate. Homeowners are not able to sell preferred equity in their home, nor are they able to seek any kind of secondary capital in their home, the way a real estate developer might seek a capital partner in an apartment complex. This is because while an apartment complex may have a single owner or be owned by a family, a building for rent is a commercial enterprise, and taking on partners in a mutually beneficial enterprise can come with rules where multiple partners have governance over the concern and the disposal of its assets. This is desirable in a business setting, where risk is fairly well understood and shared in proportion to investment, and activities are governed solely from the lens of interest-holder profit and capital preservation.

Such a direct equity partnership isn’t desirable in the context of a family home. Having to ask a co-investor in your home whether you may sell and move to a new city to accept a job opportunity or take out a second mortgage to cover an unexpected medical bill would be a bad situation for all involved. Losing the freedom to use your home as you want defeats much of the reason to be a homeowner in the first place. But the result of this dynamic is that homeowners must earn 100% of the equity portion of their home’s financing, either from savings or a family gift, and cannot seek capital partners such as the investors who are snatching up large portfolios of single-family homes all over California and the United States.

The commonplace tool of preferred equity used in commercial finance is not available to homeowners for reasons on the buy-side as well. Imagine trying to seek an outside investor in your family’s home, trying to describe what a $75,000 investment in 123 Cherry Lane will look like over ten years, what its IRR might be, the risks and downside protection. It’s preposterous to think such an asset could be originated and then sold at a global scale as is. This is not true about interest bearing debt, which performs uniformly based on an interest rate, and has an (approximate) likelihood of repayment based on the credit worthiness of the borrower. This is because debt can be secured on title with a straightforward process that doesn’t require any change in ownership, any reassessment of property values, and no hassle or conflict in the case of foreclosure or the death of an owner.

Because they can’t partner with a co-investor to help them diversify, homeowners often keep most of their wealth locked up in home equity, where it can’t be spent in local economies or contribute to their family’s fiscal life. The term “house rich, cash poor” is common parlance for a person who would, with any other asset, liquidate a portion of the growing asset to invest elsewhere in their portfolio. Without a mechanism to do this, the homeowner either borrows or does nothing, leaving capital that would otherwise be interested in owner-occupied equity exposure on the sidelines and the equity locked away.

We call this difference between the equity value locked away in a homeowner’s most important asset, and their inability or unwillingness to tap that equity with debt that would burden them with higher monthly debt service the “home equity finance gap.” We believe that bridging this gap will enable unprecedented liquidity for homeowners and a concrete solution to the decline in homeownership and its associated social benefits.

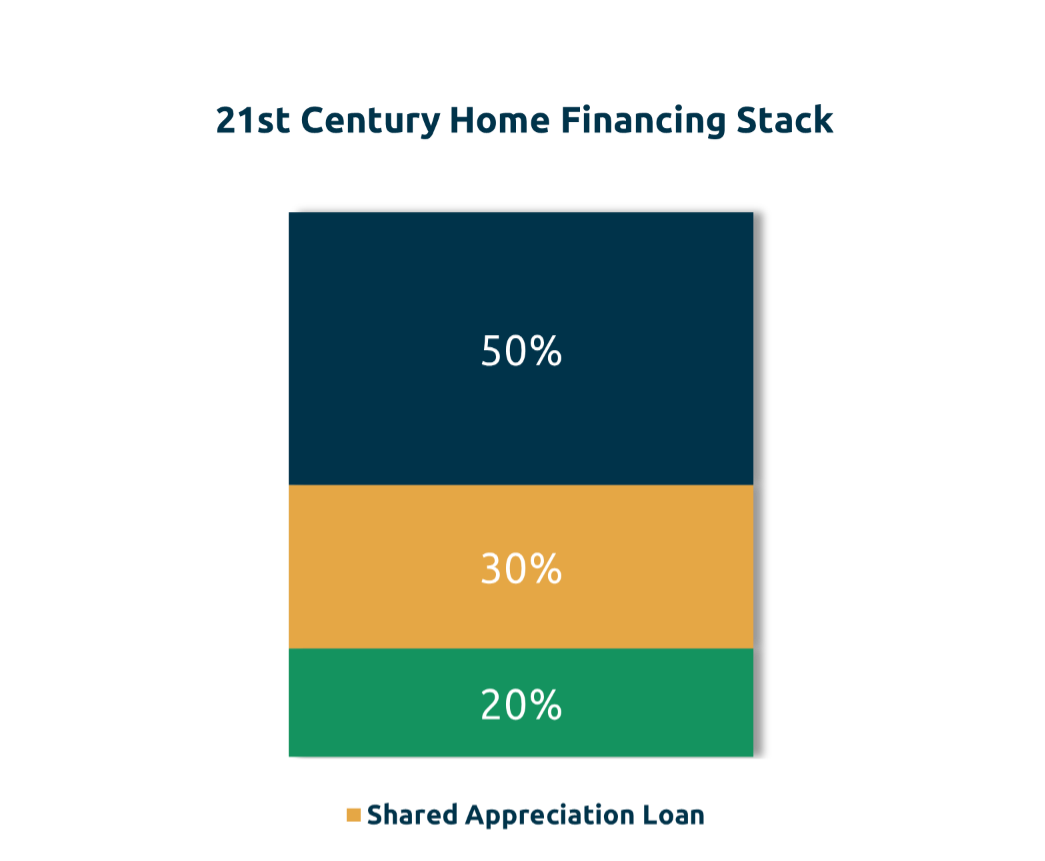

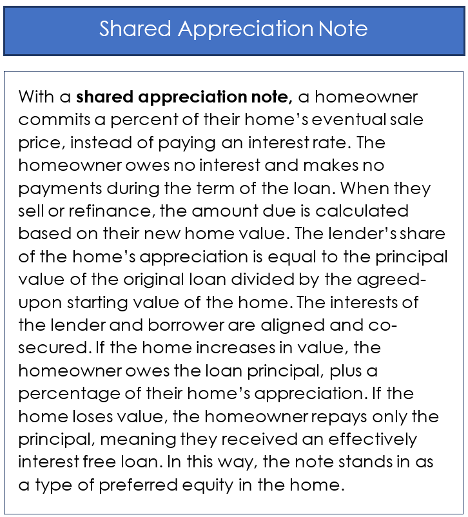

If a homeowner was able to seek a co-investor in the home’s future appreciation, but secured as debt on the home’s title, the homeowner would retain complete autonomy over the home, provided they repay their co-investor their share of the home’s value at any liquidity event like a sale or refinance. In the event a home loses value during the life of the loan, the borrower would simply repay the principal making the co-investor whole, the same way they would a holder of preferred shares of a company. An exceedingly patient investor would wait for that liquidity event for their repayment, gaining exposure to the equity appreciation of the home while staying protected on the downside by the homeowner’s share of equity. Through this model, institutional capital can find its way into the finance stacks of owner-occupied homes, buoyed by the homeowner’s remaining equity (which would be pegged to a minimum CLTV %) with security in an asset maintained and custodied by the borrower.

The question becomes how to make such a shared appreciation note attractive enough to investors to devote a sizable volume of capital and make the product available to credit-worthy homeowners across geographies and demographics. Individual notes secured by individual homes could never achieve sufficient scale, because even if the borrower’s concerns of shared ownership were solved by structuring the investment as debt, underwriting hundreds or even thousands of equity-tied loans to individual homes as a single investor would be prohibitively expensive, because the notes produced would be entirely illiquid on their own. This bottleneck in the secondary market has hindered “shared equity”-type products from achieving scale on par with the wider mortgage market. Instead, products that promise an equity partner in your home seek more stringent terms from more desperate borrowers in order to return competitive profits on their illiquid offerings to investors, who must hold them for the long term. Investors want exposure to this asset class, but their only options today demand 2-3x the return to compensate for the cost and risk inherent to selling a complex purchase option contracts to a regular homeowner.

Shared equity products will succeed only if they can take a form that investors can purchase in bulk, with a uniformity of value and risk that makes such an investment scale possible, while also deploying to the famously complex home lending market and the broad spectrum of homes, borrowers, and neighborhoods where such financing is in demand. Until now, that investability was only achievable through the commercialization of real estate assets, and securitization into existing capital markets through REITs and other public equities. But as we show above, this institutionalization cannot coexist long term with the freedom, flexibility, and social good of family homeownership.

Digital Assets and Open-Source Securitization

The advent of cryptography and the distributed ledger network protocol (or “blockchain”) has been exalted as a world shaking revolution in global finance and derided as an overhyped technology with limited practical use in the real economy that is already dead. In 2018, the World Trade Organization concluded that “the technology works best in circumstances where multiple parties are involved in transactions that require trust and transparency,” and that, “blockchain could make international trade smarter, but smart trade requires smart standardization.”

Standardization with trust and transparency in the lending market is a very good thing. Where it has been achieved — through government regulation, cooperation between banks, and the deployment of financial technology — markets have flourished. Where such standards have been lacking — such as in the run-up to the housing crisis — the opposite is true. Blockchain provides clear value to the origination and securitization of loans because the strengths of the blockchain are the same as the strengths of a well underwritten and documented mortgage investment product: standardized, trustworthy, and transparent. These tech-enabled advantages hold the key to unlocking the value of shared appreciation in owner-occupied residential real estate as a scalable investment asset. Blockchains provide a method to record transactions to a shared, tamper-proof database in real time, a tool that makes possible the instant securitization of debt and equity finance products.

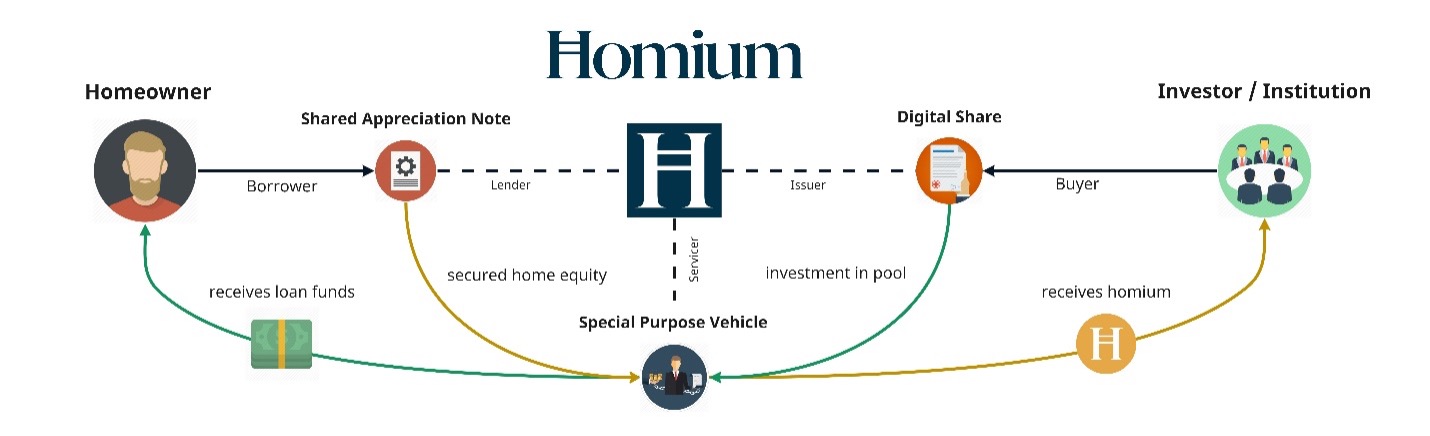

Shared appreciation notes can be securitized by ensuring the fidelity of the appraised values of onboarded homes, then by issuing a digital token that represents each dollar of home value secured. In this way, shared appreciation notes for a given lending jurisdiction (say, California) can be “tokenized” into a single, fungible, real estate-backed digital asset. For this purpose, a “token” or digital share is simply a certificated share of ownership of the special purpose vehicle or “trust” which owns the pool of notes. The trust can issue shares in itself by minting the digital share directly to investors seeking exposure to the underlying portfolio of home equity-secured notes. Each loan transaction can be standardized with a lien on title and recorded on a public blockchain, and in an easily accessible secured database so that investors know that every digital share of the pool is backed by a real dollar’s worth of home equity, in somebody’s actual home.

By offering shared appreciation notes through licensed originators, and using third-party appraisers, a purpose-built platform can provide a seamless and auditable loan origination and securitization process, and recording relevant public data on a blockchain in real-time. Investors will know the digital share holds intrinsic value from the moment of its creation, independent of speculation or the success of any one company or subset of users. Because the loan assets themselves are held and serviced by a special purpose vehicle whose cap table is entirely represented and settled through the tokenized interface, investors know that when loans are repaid, cash proceeds are exclusively used to repurchase tokens in a periodic tender offer at a variable NAV. By marking the assets in the portfolio to market value regularly, the tokenized pool becomes a secured, diversified long term equity with returns that mirror home price appreciation, but carry the low holding cost and rich, transparent data common to institutional assets.

Our Solution to the Home Equity Gap

Our company has built the technology and business ecosystem necessary for lenders to offer this product to homeowners. Our product, Homium, is a standardized and fungible digital asset backed by shared appreciation notes tied to homeowner equity. The home finance product made possible by our software platform and investor network gives homeowners a new way to access their home equity wealth without increasing the amount they pay to a bank each month, and without having to sell their home and move. It gives investors a way to deploy their capital into single family real estate without displacing homeowners from the market or transforming neighborhoods in undesirable ways. Homium’s technology shrinks the distance between the institutional investor and the homeowners, standardizing the transaction and ensuring the transparency and trust necessary for investors to hold and trade this asset at a global scale.

Investing in the shared appreciation of owner-occupied homes serves many goals of institutional investors looking for diversified real estate exposure. Homium can scale against the $7 trillion in California home equity without additional enterprise cost, because the loans that back each Homium token are offered through the same lenders who currently service the home equity loan industry. By virtue of its native digital format and complete fungibility (every Homium is the same, and represents $1 of invested real estate capital, adjusted for growth) Homium is a liquid, tradeable asset. Its nature as an open source token contract using the ERC20 standard means it can be transferred between owners at an extremely low cost, with no intervening bank or intermediary necessary to transact. This feature means that owning Homium, and by extension funding the shared appreciation notes which underly it, is much less expensive over the long term than traditional commodities or debt-backed investment products.

All of this is to say that we believe we have cracked the code to unlocking shared appreciation at scale for Californians, and we hope to soon spread this model to more jurisdictions in the US and around the world.

Homeowner Equity Partnership is Impact Investing

The shared appreciation note that backs each Homium transaction is more than just a mutually beneficial home financing arrangement, where an investor profits while a homeowner gains short term liquidity at a good price. Shared appreciation notes come with no monthly payments or interest rate, and the cash infusion represented by the investment means more money in the homeowner’s pocket with no added burden on their income or other expenses. Homeowners with money in their pockets improve their homes, pay down debt, invest in education, and pay for delayed medical care, unlocking productivity and improving their family’s wellbeing. The economies in which they participate can also receive the benefits of their added spending and capital investment, an effect that is multiplied by the added spending of those who earn that new income, a benefit that reaches homeowners and renters alike. The businesses which service homeowners, from home supply stores to childcare providers to dentists all benefit when homeowners have more money to spend without the added expense of debt service. With current untapped home equity in the United States valued at over $31 trillion, and with a current universe of consumer debt of around $5 trillion, unlocking this equity could help cover costs several times over.

The payment owed on the note is not due until a home is sold or refinanced, meaning a homeowner will not need to come up with funds to repay the loan until they have a home liquidity event themselves. The balance is then cleared through the title closing process without any action on their part. Because Homium shared appreciation lines are always in line with the borrower — for example, they receive 20% of their home’s value on day one in exchange for 20% on payoff, never more — the borrower will have no surprise and no trouble paying off the balance when the time comes. Normally, this wait would make investors disinclined to make such loans. However, the digital nature of Homium makes this liquidity inherent to the investment itself, allowing trading and continuous valuation of the Homium portfolio’s NAV, even while the bulk of loans in the portfolio are outstanding and without the expensive, centralized fund managers required to administer a traditional publicly traded security. Instead, institutions can invest at scale without liquidity risk and can hold long-term, without the fees that add drag to other investments. This benefit is borne by both the investor and the borrower and is a net positive for the economy at large.

Homeowner equity partnership via shared appreciation lending stabilizes existing homeownership and enables its growth by easing the transfer of housing wealth within the family. Homium loans are targeted at homeowners who have built up equity in their homes, stabilizing existing homeownership by removing the debt service payments associated with unlocking that equity. Homium is a more flexible alternative to restrictive reverse mortgages, which carry covenants that can drain and complicate the turnover of assets between parents and children when the time comes.

First time homebuyers may not have existing equity to unlock, but their down payments come from somewhere. 28% of FHA-insured mortgage borrowers had family assistance in 2022. Baby boomers and Gen-Xers with children entering the housing market will contribute to the down payments of the next generation. Those with greater means will rely on income and savings, but others will have to make a hard choice: borrow more, sell, or say “you’re on your own.” Homium gives parents another option, one that keeps them in their home while they help their family grow into that same stability. It lets investors cooperate with parents to finance the future without debt, and to be a silent partner to the natural transfer of equity between generations.

The cooperative nature of the Homium-compliant shared appreciation note satisfies the ethical investment standards of many social impact standards and world religions. Government-sponsored shared equity “schemes” (“program” or “offering” in the US) are gaining popularity among Muslim homebuyers and investors, because of their compliance with Sharia prohibitions on the leveling of interest. These schemes are not available to everyone even inside the UK, but their social and economic benefit can be a model for responsible and ethical home financing for people of any country or religion with private homeownership and dependable land title.

Divestment movements around the world are calling for financial institutions to move their money from extractive and harmful industries like coal mining and tobacco, and into areas where it can bolster living standards and opportunity for all people, especially working people on the cusp of economic self-sufficiency. Homium shared appreciation notes represent exactly that: a large-scale investment asset that aligns finance capital with a concrete social priority — homeowner occupied single family housing — and delivers efficient return on investment while maintaining the autonomy and quality-of-life benefits of sole ownership for the borrower. This diversifies the homeowner’s home finance stack, puts cash in their pocket to reinvest elsewhere, and lets them stay in their home instead of selling it to a private equity fund. Homium represents a divestment from the commercialization of housing and an investment into the financial independence and wellbeing of a diversified set of credit-worthy borrowers with otherwise inaccessible home equity.

A New Tool for Growth, Right When We Need It

Reasonable people can disagree on the causes and solutions to poverty, homelessness, inequality, and downward social mobility. But nearly everyone agrees that homeownership is a proven vehicle for wealth generation and housing stability. These benefits translate to improvements for children in reading abilities, lifetime incomes, incarceration rates, and life expectancies. Making homeownership easier, more flexible, and economically sustainable for both investors and homeowners is an unambiguous good, and can return a reliable profit as well.

Homium-enabled shared appreciation lending signals a tide-shift in how owner-occupied homes are financed and how institutions invest in residential real estate. An allocation of Homium in your institutional portfolio represents a stake in the rising fortunes of American families, the improvement of their schools and neighborhoods, and the flexibility and resilience of their family’s fiscal profile. Homium’s growth will coincide with the injection of millions of dollars of investor capital into homeowner bank accounts, then on to their investments in housing, education, and health, putting the world’s largest investors in the same boat as the rest of us. Now the rising tide can lift us all, together.

For more information, visit homium.io

Originally published Nov 2019, revised Nov 2021 and again in Nov 2023.